Currently, India’s repo rate stands at 6%. Consequently, the reverse repo rate under the LAF remains at 5.75%, and the marginal standing facility (MSF) rate and the Bank Rate at 6.25%

The Reserve Bank of India (RBI) will be presenting second bi-monthly monetary policy for the fiscal year FY19 at around 2.30 pm on Wednesday. RBI governor Urjit Patel along with six-member Monetary Policy Committee (MPC) for the first time in history decided to keep the policy meet for 3 days, and all eyes are now watching in what the central bank will decide for the repo rate. Many analysts have been expecting either another status quo or a rate hike in India’s policy, it need to be noted that rate cut dilemma is not in the picture. Ahead of policy announcement, the benchmark sensex index was trading at 140 points or 0.40% higher at 35,042.78, whereas the Nifty 50 is trading at 10,638.95 above 46 points or 0.43%.

Currently, India’s repo rate stands at 6%. Consequently, the reverse repo rate under the LAF remains at 5.75%, and the marginal standing facility (MSF) rate and the Bank Rate at 6.25%.

Whether rate hike or status quo, Care Ratings has laid a list of factors that will be hovering near RBI’s monetary policy decisions.

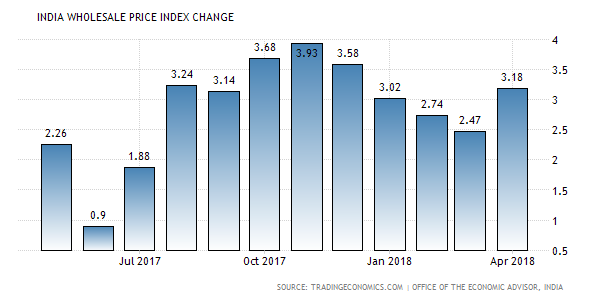

GDP

Real GDP growth improved to 7.7% in Q4FY18 compared to 7% in Q3FY18, 6.3% in Q2FY18 and three-year low number of 5.7% in Q1FY18. Such would be fastest pace of growth in seven quarters. In September 2016 quarter, India saw a growth of 7.6%.

source: tradingeconomics.com

India gets closer to its potential GDP, RBI may become more hawkish.

Inflation

Inflation has been relatively higher with CPI inflation being 4.6% and WPI inflation 3.2% in April’18.  It is largely expected that inflation will move up because – Oil prices are increasing and the government is not likely to lower duty rates. Further MSPs to be announced will lend an upward bias in prices, Prices of manufactured goods are gradually moving up indicating some recovery in pricing power, Statistically the House Rent allowance will continue to put upward pressure on CPI index.

It is largely expected that inflation will move up because – Oil prices are increasing and the government is not likely to lower duty rates. Further MSPs to be announced will lend an upward bias in prices, Prices of manufactured goods are gradually moving up indicating some recovery in pricing power, Statistically the House Rent allowance will continue to put upward pressure on CPI index.

With the rupee suddenly declining, there would be the impact of imported inflation if this lasts for long

Bank deposits and credit

During the first 2 months of any financial year, there is a tendency for both bank deposits and credit to decline. Deposits have come down by -0.3% (-1.6%) for the period March 31 to May 11, while credit has declined by -0.9% (3.2%). Therefore there has not been pressure on liquidity per se.

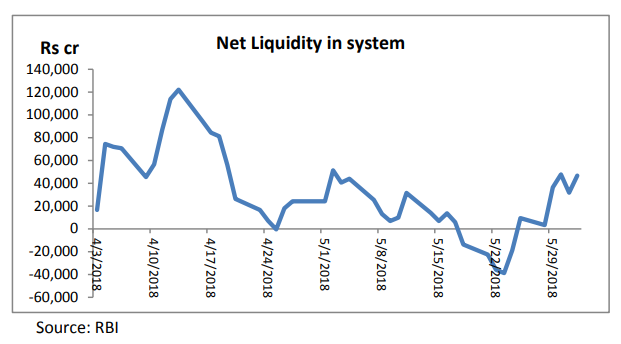

Net liquidity in the system

A good way of measuring the net liquidity in the system is to evaluate the sum effect of repos (including term repos) and reverse repos (including term reverse repos).

Government borrowing

As of June 1, the government has raised Rs 96,000 cr out of a total borrowing of Rs 6.05 lakh crore for the full year. There has not been any untoward pressure on liquidity on account of government borrowing, which implies that the RBI would be monitoring the same when announcing new auctions.

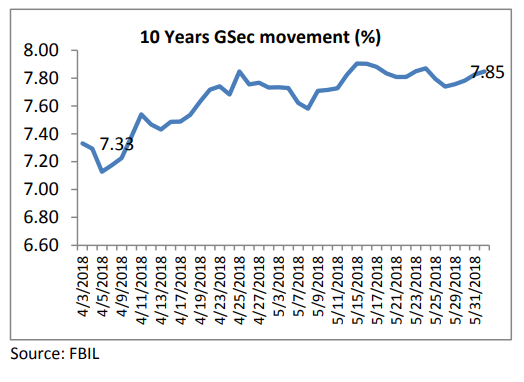

10-years GSec

GSec yields have been trending upwards from the beginning of the financial year.

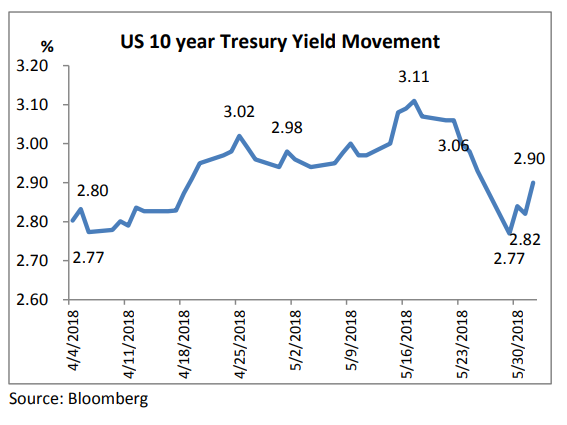

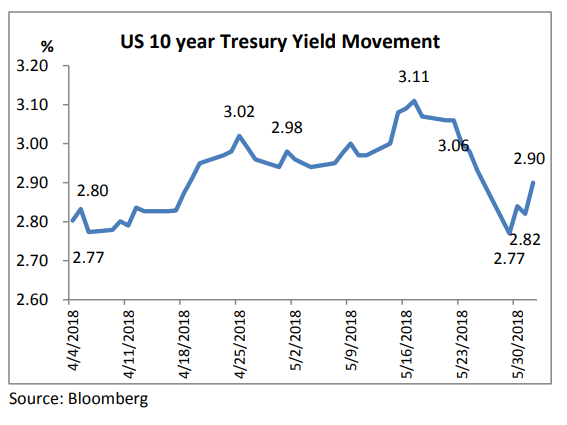

US yields have moved up and even crossed 3% which means that RBI has to keep interest rates up to ensure that FPIs retain interest in Indian markets.

FPIs

FPIs have been moving out of the country in the last two months and what is curious is that it is negative in both the equity and debt segments. Therefore, there is concern considering that the limits and tenures of investment for FPIs have been relaxed by the RBI to enable higher flows.

US rates are rising and will continue to do so

While the US economy is doing well and the unemployment rate has come down, the fear of inflation is well founded. Higher fiscal spending and tax cuts promised by the US President are likely to spook demand and generate inflationary pressures.

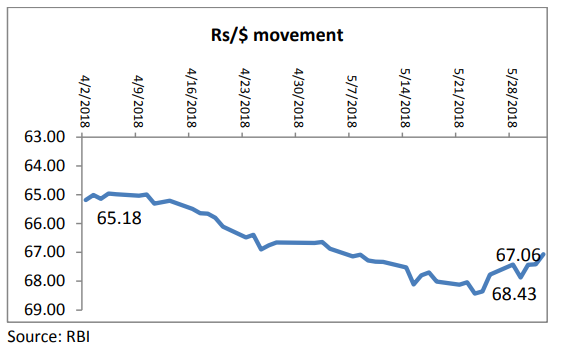

Rupee

The rupee has been falling almost continuously by almost 3% in the last two months, and also crossed the psychological mark of Rs 68/$. The oil price hike along with negative FPI flows has contributed to this phenomenon. A weaker rupee and rising interest rates in the west makes India a less attractive market for FPIs.

Considering above, economists at Care Ratings said, “With no additional data point on inflation, inflationary expectations would play an important role. These would only be in the upward direction. Therefore, there would be no rate change this time. The tone would be hawkish and this would likely to be the consensus among the members.”

They added, “There could be an upward revision in inflationary projections for the year. The April policy projected CPI inflation of 4.7-5.1% for H1 and 4.4% in H2. The first half projection is to be revised upwards to 4.9%-5.1% and H2 to 4.6%. CRR and SLR not to be changed. Banks have excess SLR of almost 8% presently.”

{kind=link}